Strategy Introduction

This section outlines a mean-reversion strategy designed for the daily timeframe. The system seeks to identify short-term price dislocations within the crypto market and capitalize on temporary deviations from typical price levels.

The strategy operates on the principle that markets frequently experience brief periods of overextension caused by volatility and short-term sentiment shifts. When such conditions occur, prices may move excessively away from their recent equilibrium. The system attempts to exploit these moments by entering long positions when price action indicates an unusually sharp downward move relative to recent market behavior.

Because the strategy focuses on short-term market inefficiencies rather than sustained directional trends, trades are generally intended to capture quick rebounds following temporary selling pressure. As a result, positions are typically held only for a short period, with exits triggered once price action begins to normalize or momentum shifts against the position.

Due to the long-only structure, the strategy is specifically designed to benefit from short-term recoveries in the crypto market rather than profiting from declining prices.

All signals, entries, and exits are fully systematic and governed by a predefined rule set, ensuring that the strategy operates mechanically and without discretionary intervention.

Strategy Description

The strategy identifies short-term price dislocations by combining measures of price weakness and volatility expansion within a broader market context.

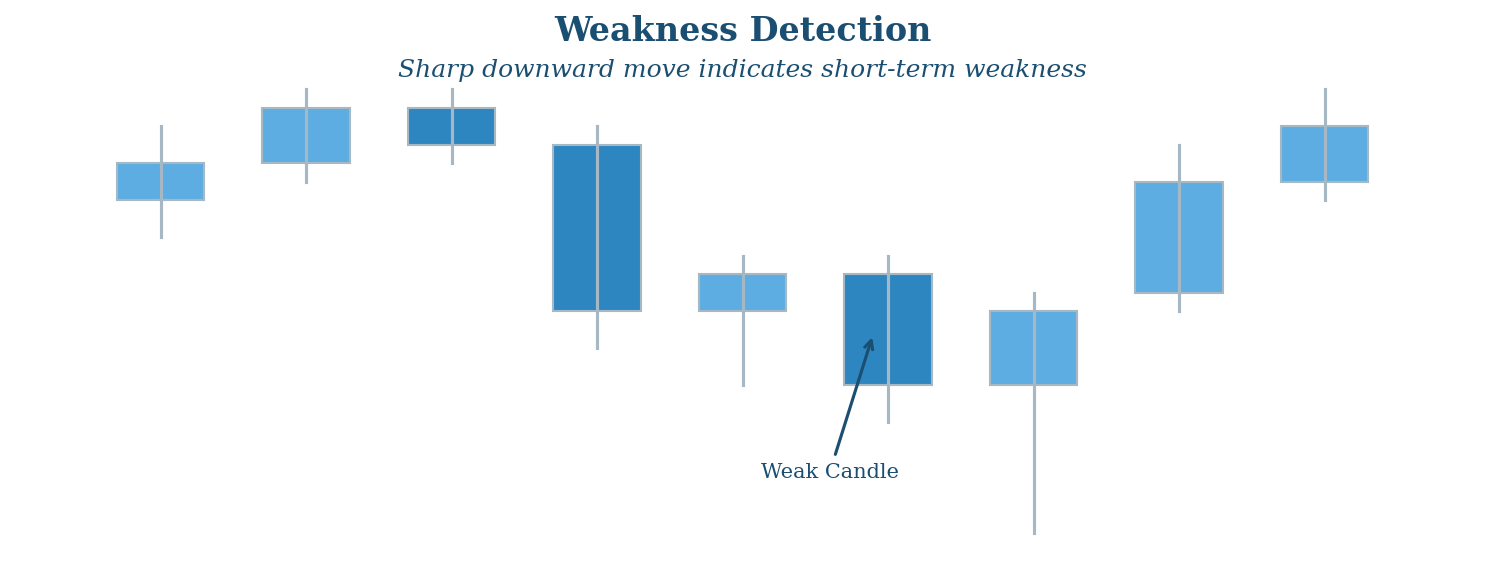

Short-term weakness is detected when the current closing price falls below the previous day’s low. This condition signals a breakdown in recent price structure and indicates that selling pressure has accelerated beyond typical day-to-day fluctuations.

To ensure that such moves are meaningful, the strategy incorporates a volatility filter. Specifically, short-term volatility – measured by a short-horizon Average True Range (ATR) – must exceed longer-term volatility. This requirement ensures that signals are only generated during periods of elevated market activity, where price dislocations are more likely to occur.

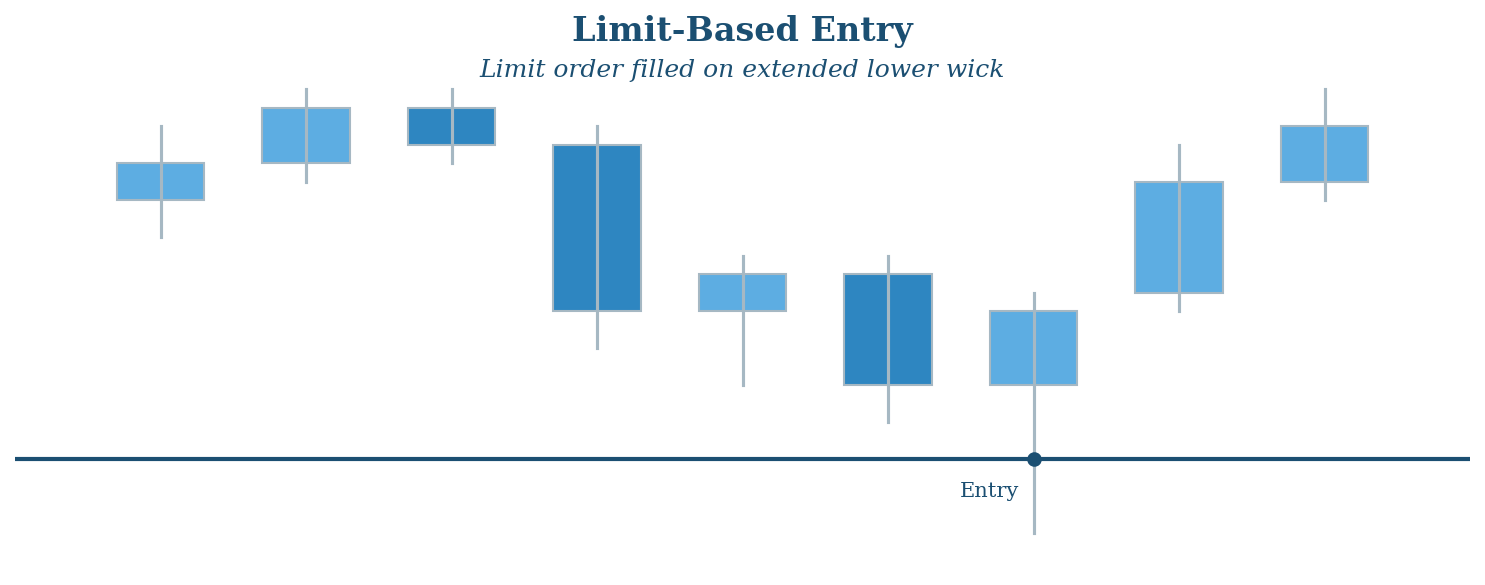

Once these conditions are met, positions are not entered immediately at market price. Instead, the strategy places a limit order below the current low, offset by a fraction of the short-term ATR. This entry mechanism requires further downside extension before execution, allowing the strategy to enter at more extreme price levels and improving the expected mean-reversion potential.

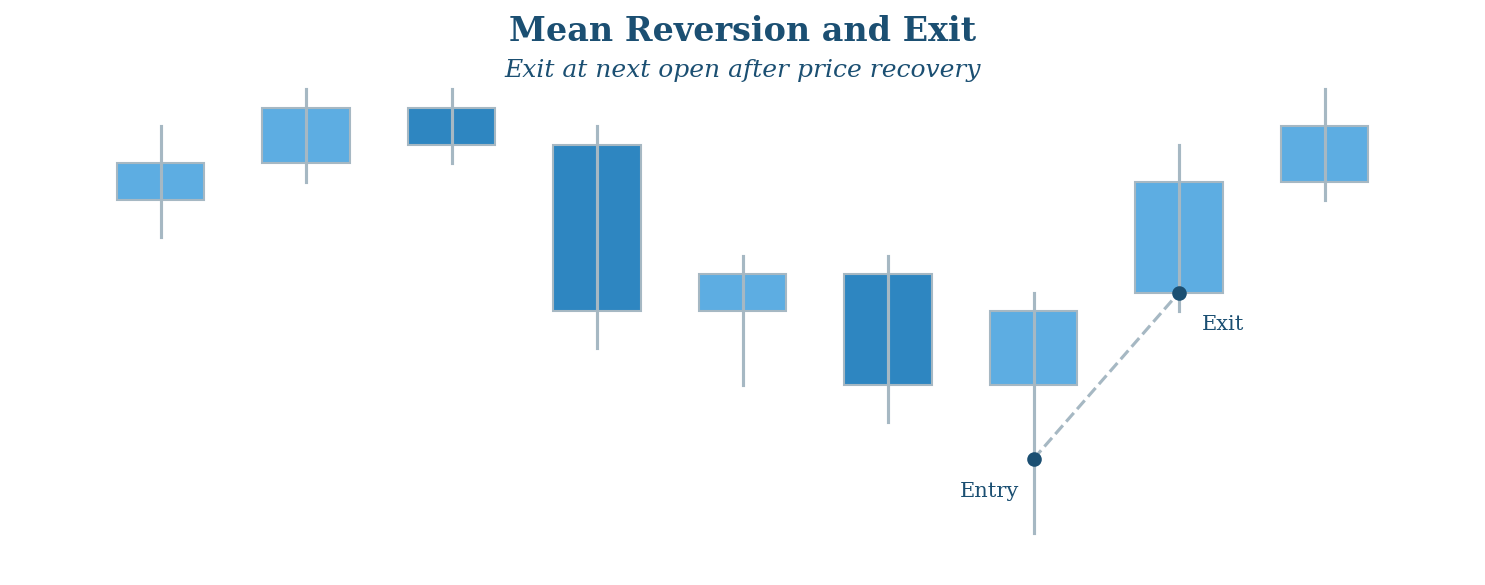

Positions are managed with a short holding horizon. Exits are triggered either when price recovers above the average entry level—indicating a successful rebound—or when price weakens further relative to a short-term moving average, signaling that the anticipated reversion has failed.

Conclusion

This example illustrates how short-term price dislocations are systematically identified and traded using a mean-reversion framework. By entering positions after sharp downward moves and exiting as prices recover, the strategy aims to capture temporary deviations from typical price levels.

Due to this approach, the strategy typically exhibits a relatively high win rate, as many trades benefit from quick rebounds following short-term selling pressure. In addition, positions are generally held only for a short period, reflecting the transient nature of these market inefficiencies.

The effectiveness of the strategy is based on the tendency of markets to overreact in the short term. Periods of elevated volatility and abrupt price declines often lead to temporary oversold conditions, which are subsequently followed by partial recoveries. By systematically targeting these situations, the strategy seeks to exploit recurring mean-reversion behavior in the market.